Retirement is sold as the calmer chapter, yet the rules keep running in the background. Benefits programs, tax deadlines, and health coverage all assume steady compliance, even when life slows down and routines change.

Legal advisers say penalties rarely start with bold choices. They start with ordinary moments: a pill offered to a spouse, a surprise medical shipment left unreported, or a small gig treated as too minor to mention. The shock comes later, as a letter demanding repayment, a benefit pause, or fees that feel like they appeared overnight. A few simple checks, done monthly, keep life steady. Calm grows when details stay in order now.

Sharing Leftover Prescription Pills

An extra pain pill in the cabinet can look like a simple favor, yet many prescriptions are controlled substances. Those rules are built to keep dispensing tied to a licensed prescriber and a named patient, not to good intentions or family convenience.

Legal advisers warn that handing a controlled prescription to another person can be treated as unauthorized distribution, even when no money changes hands. Trouble often starts later, when a refill check, insurance review, or medical complication raises questions. The safer habit is to keep leftovers secured, ask a pharmacist for options, and use a take-back program for disposal when available.

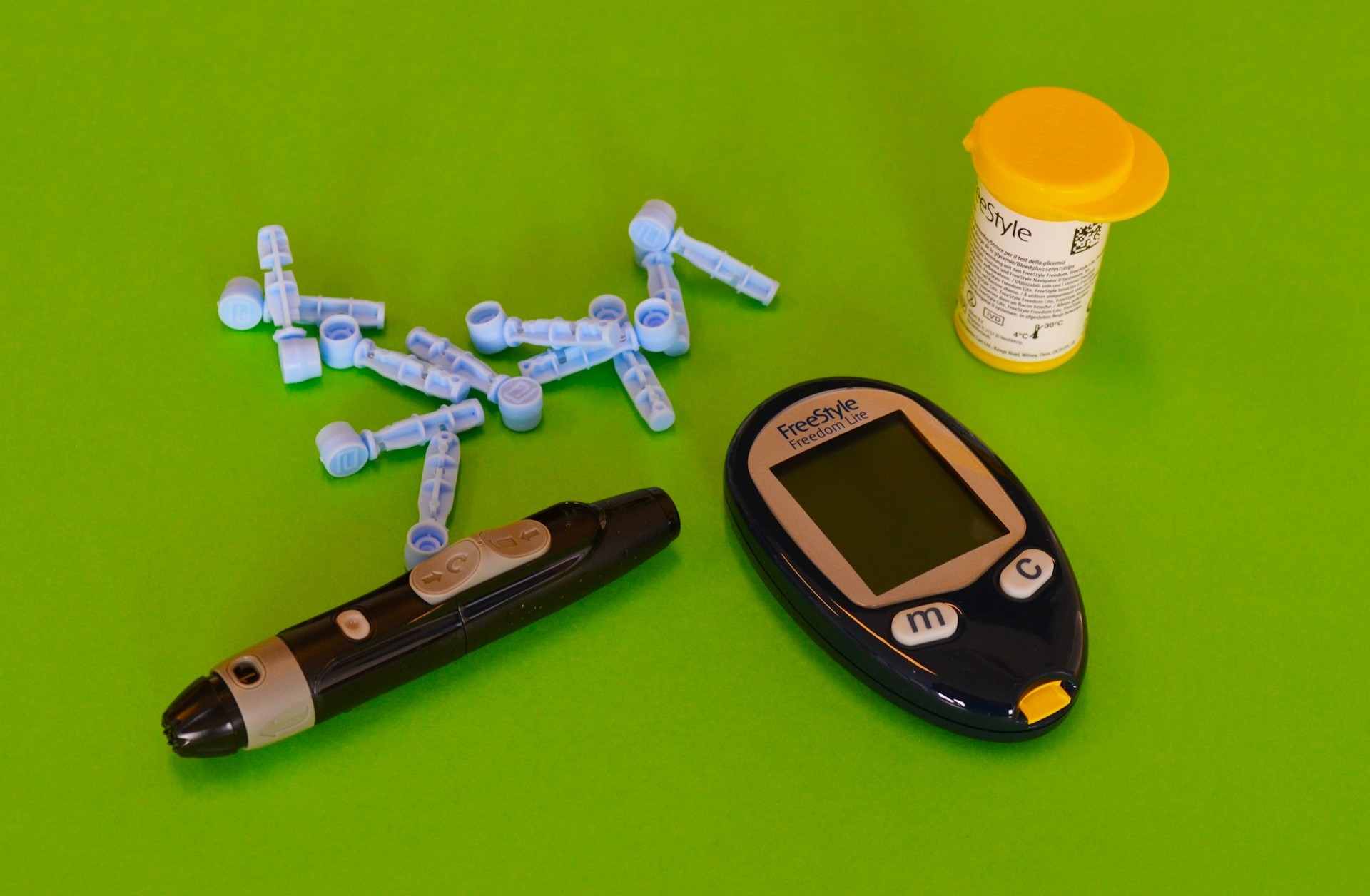

Keeping Unrequested Medical Equipment

Unordered braces, catheters, or diabetic supplies sometimes arrive with paperwork that looks official. Scammers count on that moment of doubt, then bill Medicare under the beneficiary’s name, hoping the box is kept and the statement is ignored.

Senior Medicare Patrol guidance flags this as a common durable medical equipment scheme. It recommends matching Medicare Summary Notices and plan Explanation of Benefits forms to real appointments and actual orders, then reporting anything that does not line up. Fast reporting helps reverse claims, limits future misuse of the Medicare number, and shows there was no consent to the charge.

Earning On SSDI Without Reporting

Some retirees on SSDI take small jobs for routine, social contact, or extra income, assuming a few shifts will not matter. SSA rules do allow work, but the system hinges on self-reporting and hard monthly thresholds that change over time.

In 2026, a trial work month is counted when earnings exceed $1,210, and substantial gainful activity for non-blind beneficiaries is $1,690 a month. When earnings are not reported, overpayments can pile up quietly, then arrive as repayment demands or benefit changes. Keeping pay stubs, reporting quickly, and confirming how the job is treated prevents a small gig from turning into a long paper chase.

Treating A Side Hustle Like A Hobby

Selling baked goods, tutoring, or online crafts can feel like a casual retirement project. Once sales become regular, local licensing, permits, zoning rules, and sometimes health codes can apply, and the line is different in each county and city.

Federal rules can still follow even when the work feels small, because business income is generally reportable and platform tax forms can surface it later. Legal planners often suggest checking permit needs early, keeping simple logs of sales and expenses, and separating the money in its own account. That basic setup can prevent backdated fees, surprise fines, or a shutdown after a complaint.

Missing Required Minimum Distributions

RMD rules are a calendar trap because accounts sit quietly for decades, then suddenly demand action. For many tax-deferred retirement accounts, the IRS generally requires distributions to begin at age 73, even if the money is not needed yet.

Missing the full withdrawal by the due date can trigger an excise tax on the shortfall: 25%, or 10% if the mistake is corrected within 2 years, typically reported on Form 5329. The first-year timing can also create a double-withdrawal year if delayed into spring, raising taxable income. A dated reminder for every account keeps forgotten plans from becoming expensive surprises, with penalties avoided.